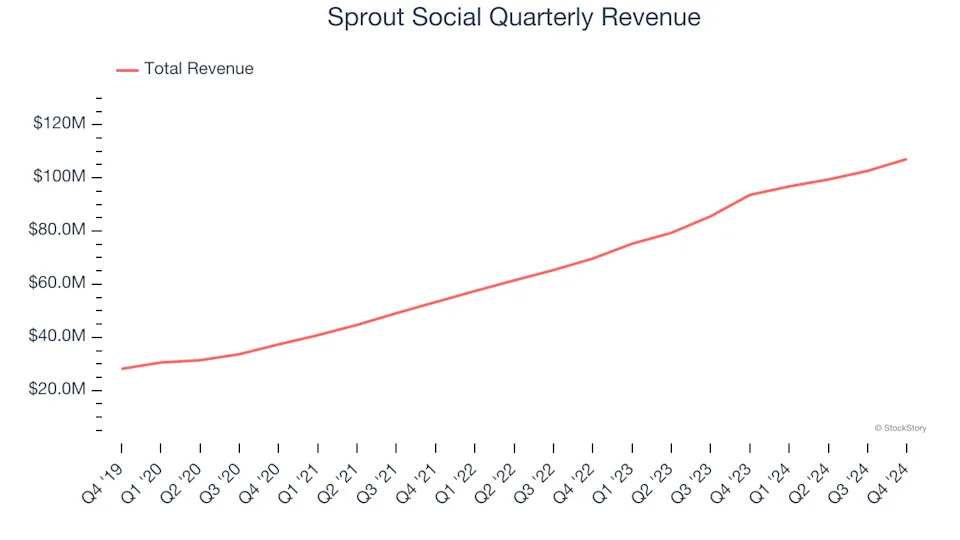

Social media management software company Sprout (NASDAQ:SPT) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 14.4% year on year to $107.1 million. On the other hand, next quarter’s revenue guidance of $107.6 million was less impressive, coming in 2.2% below analysts’ estimates. Its non-GAAP profit of $0.19 per share was 25.4% above analysts’ consensus estimates.

Is now the time to buy Sprout Social? Find out in our full research report .

Sprout Social (SPT) Q4 CY2024 Highlights:

“The Sprout team delivered a solid fourth quarter, driving 14% revenue growth and 26% growth in cRPO, laying the foundation for future growth in 2025 and beyond. As we work to define the future of social media management, we remain focused on execution—winning the enterprise, driving customer health, expanding our partnership ecosystem, and driving deeper engagement in our customer base,” said Ryan Barretto, CEO.

Company Overview

Founded by Justyn Howard and Aaron Rankin in 2010, Sprout Social (NASDAQ:SPT) provides a software as a service platform that companies can use to schedule and respond to posts on major social media networks like Twitter, Facebook, Instagram, Youtube and LinkedIn.

Marketing Software

Whether or not companies market their products through social media, all businesses need to meet customers where they are; and increasingly, that is social media. As more and more people use a greater number of social media platforms, social media management software become more valuable to their customers.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Sprout Social’s sales grew at an impressive 29.3% compounded annual growth rate over the last three years. Its growth beat the average software company and shows its offerings resonate with customers.

This quarter, Sprout Social’s year-on-year revenue growth was 14.4%, and its $107.1 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 11.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 14.3% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is healthy and suggests the market is factoring in success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

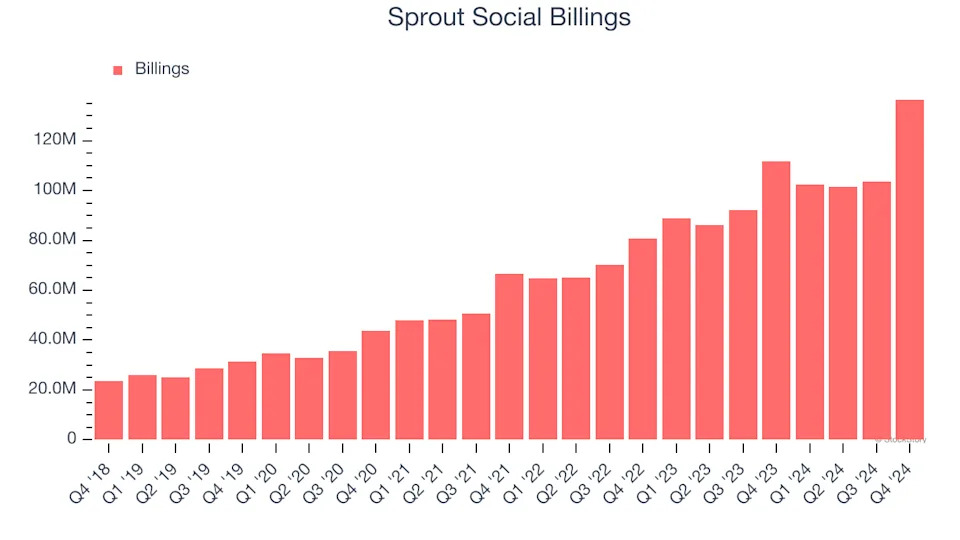

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Sprout Social’s billings punched in at $136.6 million in Q4, and over the last four quarters, its growth was solid as it averaged 17% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

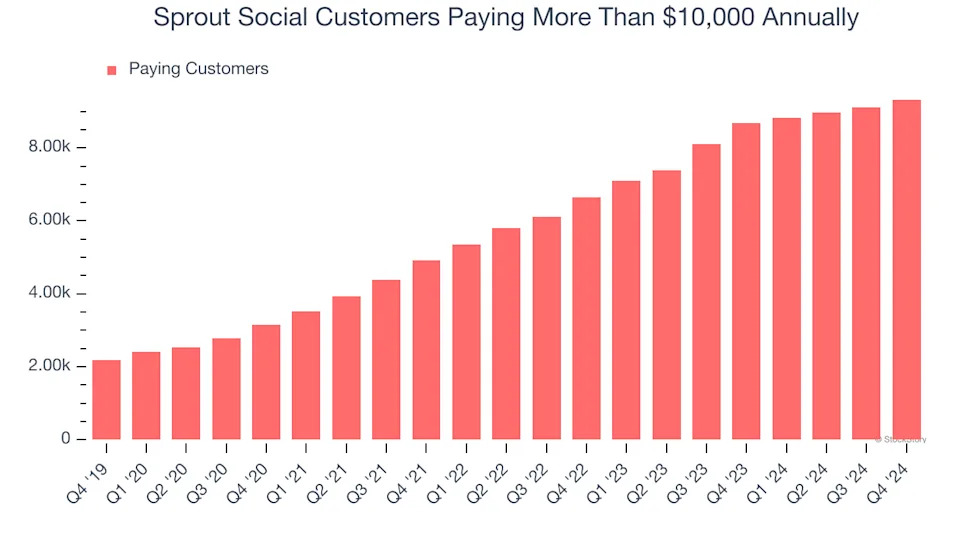

Enterprise Customer Base

This quarter, Sprout Social reported 9,327 enterprise customers paying more than $10,000 annually, an increase of 208 from the previous quarter. That’s quite a bit more contract wins than last quarter but also quite a bit below what we’ve observed over the previous year. This indicates the company is optimizing its go-to-market strategy to reinvigorate growth.

Key Takeaways from Sprout Social’s Q4 Results

We were impressed by how significantly Sprout Social blew past analysts’ billings expectations this quarter. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand and it fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 6.9% to $25.40 immediately after reporting.

So should you invest in Sprout Social right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .