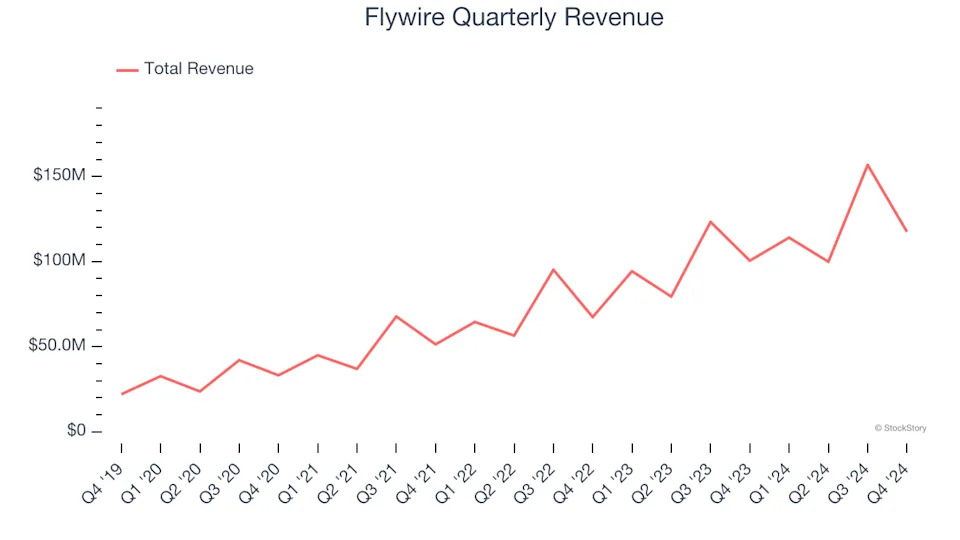

Cross border payment processor Flywire (NASDAQ: FLYW) missed Wall Street’s revenue expectations in Q4 CY2024, but sales rose 16.9% year on year to $117.6 million. Next quarter’s revenue guidance of $127.2 million underwhelmed, coming in 8.7% below analysts’ estimates. Its GAAP loss of $0.12 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Flywire? Find out in our full research report .

Flywire (FLYW) Q4 CY2024 Highlights:

"Our fourth quarter results capped off another strong year for Flywire as we continued to grow the business while navigating a complex macro environment with significant headwinds,” said Mike Massaro, CEO of Flywire, “We continued to focus on business and bottom line growth and generated 17% revenue growth and 680 bps adjusted EBITDA margin growth in the quarter.”

Company Overview

Originally created to process international tuition payments for universities, Flywire (NASDAQ:FLYW) is a cross border payments processor and software platform focusing on complex, high-value transactions like education, healthcare and B2B payments.

Payments Software

Consumers want the ability to make payments whenever and wherever they prefer – and to do so without having to worry about fraud or other security threats. However, building payments infrastructure from scratch is extremely resource-intensive for engineering teams. That drives demand for payments platforms that are easy to integrate into consumer applications and websites.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Flywire’s sales grew at an excellent 34.4% compounded annual growth rate over the last three years. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

This quarter, Flywire’s revenue grew by 16.9% year on year to $117.6 million but fell short of Wall Street’s estimates. Company management is currently guiding for a 11.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 23.9% over the next 12 months, a deceleration versus the last three years. Still, this projection is admirable and suggests the market sees success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

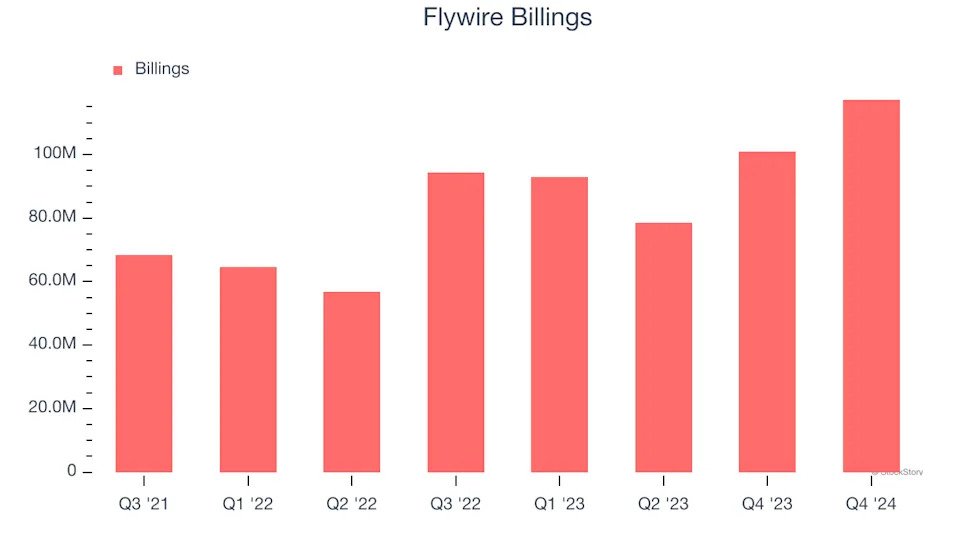

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Flywire’s billings punched in at $117.2 million in Q4, and over the last four quarters, its growth was solid as it averaged 16% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Flywire’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from Flywire’s Q4 Results

It was good to see Flywire narrowly top analysts’ EBITDA expectations this quarter. On the other hand, its revenue guidance for next quarter missed significantly and its revenue for this quarter also fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 17.1% to $14.63 immediately after reporting.

Flywire’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .